For many small businesses, cash flow is the foundation that keeps operations alive. Payroll, inventory purchases, rent, taxes, marketing expenses, vendor payments, and customer fulfillment all depend on maintaining consistent access to working capital.

When daily cash flow becomes unstable, even profitable businesses can quickly experience operational distress.

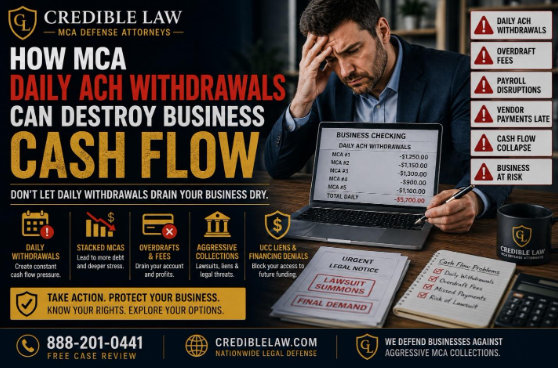

This is one reason merchant cash advance (MCA) repayment structures have become increasingly controversial among business owners nationwide. While MCAs are often marketed as fast and flexible financing solutions, many businesses eventually discover that aggressive daily ACH withdrawals can place extraordinary pressure on operating accounts.

Across industries such as:

-

trucking,

-

eCommerce,

-

retail,

-

construction,

-

hospitality,

-

and professional services,

companies are reporting growing financial strain tied to overlapping MCA withdrawals, stacked advances, and escalating collection activity.

For many owners, the issue is not simply the amount borrowed — it is the speed and frequency of repayment extraction from the business account itself.

How MCA ACH Withdrawals Work

Unlike traditional loans that typically involve monthly payments, many MCA agreements authorize:

-

daily ACH debits,

-

weekly remittances,

-

or recurring withdrawals tied to estimated receivables.

These withdrawals often begin almost immediately after funding is deposited.

In theory, the structure is designed to allow MCA companies to collect payments gradually based on business performance. In practice, however, businesses frequently report that daily ACH withdrawals create severe operational instability once revenues fluctuate or multiple advances become stacked simultaneously.

Even small interruptions in revenue can create cascading problems when fixed withdrawals continue processing every business day.

Why Daily Withdrawals Create Operational Pressure

Most businesses experience natural fluctuations in revenue.

Sales cycles change. Customers delay payments. Seasonal slowdowns occur. Expenses rise unexpectedly.

Traditional financing structures generally allow businesses time to adapt to these fluctuations through predictable monthly repayment schedules.

Daily MCA withdrawals often provide far less flexibility.

Businesses facing multiple daily withdrawals may experience:

-

constant overdrafts,

-

declining operating balances,

-

failed payroll transactions,

-

vendor payment delays,

-

bounced checks,

-

and mounting bank fees.

Over time, the company may begin operating almost entirely to satisfy lender withdrawals rather than sustaining healthy business growth.

The Dangers of MCA Stacking

One of the biggest contributors to cash flow collapse involves MCA stacking.

Stacking occurs when businesses obtain additional advances while prior positions remain active.

Businesses often pursue stacked funding because:

-

daily withdrawals become difficult to sustain,

-

operational expenses increase,

-

taxes come due,

-

or traditional financing becomes unavailable.

Initially, new capital may temporarily relieve pressure.

But each additional position compounds:

-

ACH obligations,

-

repayment exposure,

-

lender conflicts,

-

and operational instability.

Eventually, many businesses reach a point where incoming revenue is consumed almost entirely by overlapping withdrawals before essential operating expenses can even be addressed.

This creates a dangerous financial cycle that becomes increasingly difficult to escape.

Why Businesses Begin Falling Behind

Many business owners do not anticipate how quickly MCA obligations can escalate.

What initially appears manageable may become unsustainable after:

-

seasonal revenue declines,

-

inventory disruptions,

-

customer payment delays,

-

or rising operating expenses.

Because ACH withdrawals continue processing regardless of temporary business conditions, companies may suddenly find themselves:

-

struggling to cover payroll,

-

unable to maintain vendor relationships,

-

or facing repeated account overdrafts.

At that point, some businesses seek additional advances simply to maintain operations, which often worsens the underlying problem further.

Aggressive Collections Often Follow Payment Problems

Once ACH withdrawals begin failing or payments become inconsistent, collection activity may escalate quickly.

MCA companies may pursue:

-

intensified withdrawal attempts,

-

lawsuits,

-

arbitration proceedings,

-

UCC enforcement,

-

personal guarantee claims,

-

or aggressive collection demands depending on the agreement structure and governing law.

Businesses carrying multiple active positions may suddenly face simultaneous pressure from several funders at once.

This often creates enormous operational and emotional stress for business owners attempting to keep the company functioning.

Businesses experiencing escalating collection activity frequently seek guidance from experienced Merchant Cash Advance Defense Attorneys to evaluate agreements, assess collection exposure, and determine whether restructuring or defense strategies may exist.

The Role of Reconciliation Provisions

Many MCA agreements contain reconciliation provisions intended to adjust payments based on actual receivables performance.

However, disputes frequently arise regarding:

-

whether reconciliation rights were properly honored,

-

how payment calculations were performed,

-

or whether withdrawals accurately reflected business revenue.

Businesses experiencing declining sales sometimes continue facing aggressive ACH withdrawals despite contractual language suggesting payments should fluctuate with receivables performance.

Understanding how reconciliation rights operate within the agreement can become extremely important once operational pressure begins increasing.

UCC Liens and Financing Denials

Cash flow instability caused by MCA withdrawals often becomes even more damaging when combined with UCC liens.

Many MCA providers file UCC financing statements shortly after funding.

These filings can affect:

-

future lending opportunities,

-

refinancing efforts,

-

SBA loan approvals,

-

equipment financing,

-

and overall business creditworthiness.

Businesses often discover the seriousness of these filings only after traditional lenders decline financing applications due to existing MCA exposure and stacked obligations.

For companies attempting to refinance into more stable financing products, multiple active UCC filings can become a major obstacle.

Why Businesses Wait Too Long

One of the most common mistakes businesses make is delaying action while hoping revenues will improve enough to stabilize operations.

Owners often assume:

-

another good sales month will solve the issue,

-

lenders will cooperate informally,

-

or additional funding will create breathing room.

Unfortunately, by the time lawsuits, account restraints, or severe collection activity begin, available options are often far more limited.

Early review may help businesses:

-

evaluate restructuring opportunities,

-

assess reconciliation disputes,

-

stabilize cash flow,

-

negotiate resolutions,

-

or preserve leverage before litigation escalates further.

Businesses facing mounting ACH pressure frequently begin researching resources related to Merchant Cash Advance Lawsuits while attempting to understand the legal and financial risks associated with their agreements.

The Emotional Impact on Business Owners

The pressure associated with daily MCA withdrawals extends beyond business finances alone.

Entrepreneurs often report:

-

chronic anxiety,

-

inability to sleep,

-

fear of losing the company,

-

strained relationships,

-

and overwhelming uncertainty regarding future operations.

Business owners who spent years building their companies may suddenly find themselves trapped in a cycle of escalating obligations and aggressive collections.

This emotional pressure can sometimes lead businesses into rushed financial decisions that worsen the situation further.

Final Thoughts

Merchant cash advances can provide rapid access to capital, but daily ACH repayment structures may create severe operational risks when revenues fluctuate or multiple advances become stacked simultaneously.

Businesses nationwide are increasingly reporting:

-

cash flow collapse,

-

financing denials,

-

aggressive collections,

-

UCC complications,

-

and litigation exposure tied to MCA obligations.

Understanding the long-term impact of daily ACH withdrawals before the situation escalates further can play a critical role in protecting operational stability and preserving the future of the business.

For companies already experiencing mounting pressure, early evaluation of agreements, repayment structures, and collection exposure may significantly affect available options moving forward.